🌌 Reshaped #39

Green VCs, climate policy tradeoffs, European startup ecosystems, gig (un)regulation and much more

Welcome to a new issue of Reshaped, a newsletter on the social and economic factors that are driving the huge transformations of our time. Every Saturday, you will receive my best picks on global markets, Big Tech, finance, startups, government regulation, and economic policy.

No worries: this issue is not about the US elections. I also tried to keep it shorter than usual. Climate change is the common line that links most of the topics covered in this issue. As governments started to embed climate policy in their national industrial strategy, actors in the innovation economy hope that new investment opportunities will arise in the greentech sector. Expect more space dedicated to these issues in the upcoming weeks!

Please, take a moment to share this newsletter with your network!

New to Reshaped? Sign up here!

The state

Climate policy

In Norway, environmental groups complained about the domestic energy policy, “built around an oil and gas industry that accounts for more than half of national exports” (The New York Times). These groups aim to “invalidate licenses for new oil exploration in the Arctic”, claiming that oil drilling activities violate the constitutional right to a healthy environment. This is not the first case in which environmentalists push for a more ambitious climate policy, but the use of human rights as a lever for such a radical shift can create an important precedent in environmental law. Domestic media defined it the case of the century, especially for its potential economic effects.

Notoriously, Norway’s climate policy is a paradox. On one hand, it is a champion in the fight against climate change; on the other, it is trying to expand its oil drilling operations in the Arctic (see picture below), which raises concerns about local ecosystems and foreign relations with Russia (The Guardian).

As more and more states worldwide commit to stricter climate policies, this kind of inconsistencies arise as a consequence of the slow implementation of green best practices and the lack of a true systemic approach — however banal it may sound. A recent article on Nature explains how the European Green Deal simply ends up offshoring the environmental damage to other countries (very recommended read).

First, the EU depends heavily on agricultural imports; only China imports more. […] This enables Europeans to farm less intensively. Yet the imports come from countries with environmental laws that are less strict than those in Europe. And EU trade agreements do not require imports to be produced sustainably. […] The net result? EU member states are outsourcing environmental damage to other countries, while taking the credit for green policies at home. Although the EU acknowledges that some new legislation will be required around trade, in the short term, nothing will change under the Green Deal.

This is particularly relevant as a new study published on Science explains that any climate policy that fails to address global food emissions “could preclude achieving the 1.5° and 2°C climate change targets”. Even supposing a virtuous path towards green manufacturing, transportation, and energy production, the lack of appropriate measures to reduce food emissions would break the 1.5°C target between 2051 and 2063.

For a holistic approach towards a green transition in the US, some argue that it is necessary to launch an ambitious National Energy Innovation Mission (MIT Technology Review). The starting point is clear: we need to invest more in new technologies and their commercialization to achieve our climate objectives. This makes sense as it would help to boost private investments in the field.

Critical for a global clean-energy transition, these include technologies that will help us capture and store carbon emissions from the atmosphere and fossil-fuel plants; produce and use clean fuels such as hydrogen; store variable wind and solar power for long durations; manage complex systems such as smart electricity grids; and more. Roughly half the reductions required to swiftly reach global net-zero emissions must come from technologies that aren’t yet commercially available.

The markets

European startups

Dealroom and Sifted recently released an interesting report that explores the main trends in the European startup ecosystem. Some insights:

The European share of global VC investments has been growing during the last decade and is expected to account for 15% in 2020.

Europe leads in seed investments but lacks appropriate growth capital; foreign investors are still fundamental to finance bigger rounds.

Startups are the fastest growing engines of job creation in Europe, with a 10% annual growth rate.

European startups are, on average, less focused on commercial applications than their foreign counterparts.

France is the country that invested the most in supporting domestic startups during the pandemic (see picture below).

Gig economy

After a long legal battle, Uber, Lyft, and Doordash will be allowed to continue to treat their drivers as independent contractors instead of employees (The New York Times). The approval of Proposition 22 will “exempt the companies from a state labor law that would have forced them to employ drivers and pay for health care, unemployment insurance, and other benefits” and will allow them “to remake labor laws throughout the country”. What Kate Conger fears, of course, is that the widespread adoption of gig economy business models will negatively impact working conditions.

According to Nicolas Colin, however, the solution lies not in preventing the gig economy from spreading but in building an appropriate social contract to protect these workers and promote entrepreneurship (Sifted).

It’s not that hard to figure out what that new social contract would look like. Basically, it would cover workers against the new risks of the day, like the impossibility of affording housing in urban areas when your revenue stream is derived from gig platforms (good luck reassuring a landlord with that!). It would provide access to capital when and where you need it, which wouldn’t necessarily be to buy a car (a thing of the past), but instead to learn new skills when it’s time to move on in your life. And it would help workers organise so that they defend their interests themselves, but with a different approach from that which was embraced in the coal mines of the 19th century or the car factories of the 20th.

According to Uber CEO Dara Khosrowshahi, this achievement “should serve as a template for regulating the gig economy in other states and nations” (Politico).

Big Tech

I have some interesting reading recommendations regarding tech companies:

The relationship between Apple and Foxconn, its most important manufacturing partner, has recently become unsustainable for the latter, which tried to stay afloat through (incredibly) unfair practices (The Information).

Frank Pasquale wrote a beautiful essay on emotion detection technologies and their controversial applications (Real Life).

On The Markup, Colin Lecher analyzed how tech companies behaved during the US elections.

The speculators

Venture capital

According to The Economist, VC funds are increasingly focusing on climate-related technologies. In 2019 they set a record, with $36 billion invested in green ventures, and this year they can even surpass it.

Half the money flowed into North American startups […]. China accounted for between 15% and 30%, depending on how the sector is defined, and Europe for another 15%. This should spur innovation and, hopefully, lower the relative price of climate-friendly technology even in the absence of regulations making carbon-heavy ones dearer. And it needs to happen across the board, not just in energy and transport. […] About half the deals by value go to low-carbon transport, encouraged by Tesla’s credulity-stretching success.

This interest by VC funds is motivated by two recurring factors in the innovation economy. On one hand, there is a growing commitment to reduce carbon emissions by governments all around the world. This helps to reduce overall risk (see my past issue on that topic) and makes long-term investments more attractive. On the other hand, climate-related stocks are performing well in public markets, which will make it easier to find exit opportunities. However, more effort is required to boost demand for these technologies and, once again, public purchasing might prove fundamental to mitigate the risks of excessive market fragmentation. As the article correctly points out, “targeted government procurement could boost green products, as happened when the Pentagon enlisted Silicon Valley to make computers”.

Investment banking

A new report by CB Insights explores the disruption occurring in the investment banking industry. In particular, the changes occurring in the IPOs process are the most impactful driver of this disruption.

[…] the powerful tech companies fueling the world’s biggest IPOs are exerting their influence, using their size and name recognition to extract lower fees from the investment banks. Some are also exploring alternatives to the IPO, like the direct public offering (DPO) and alternative exchanges. And perhaps the trend that’s had the biggest impact — some big companies are electing not to go public at all. Thanks in part to an abundance of cash being offered by venture capitalists and sovereign wealth funds, many startups are opting to stay private indefinitely. As a result, investment banks are having to chase more deals and reaping lower revenues for doing so.

Investment banks are investing in digital technologies and blockchain to stay afloat. However, due to the falling fees and their negative impact on revenue growth, some kind of business model shift is to be expected at least on the cost structure side.

IPOs

Surprisingly, the long-awaited Ant IPO was suspended by Chinese authorities, which required more time to scrutinize the company and the high-growth domestic fintech sector (Bloomberg). According to these authorities, the company will face intensive regulation that will force it to adapt its business model in many ways. According to Marc Rubinstein, this shows a relevant shift in regulatory practices.

Ant has for a long time been keen to distance itself from financial services and cosy up with tech, first by categorising itself as a “techfin” and then by dropping “Financial” from its name. However, regulators are equally keen for this not to happen and can be quick to drag the company back under their purview. It’s the same all over the world. Having spent many years post the financial crisis looking inwards, financial regulators are now looking outwards.

This is a disaster for Ant, which will have to refund all of its institutional investors and, in the most optimistic scenario, delay its $34.5 billion IPO. But it is also bad news for Chinese markets, which saw in this record-setting public listing a chance to close the gap with US markets in terms of high-rewarding tech IPOs. Moreover, the delay will hurt the various investment banks involved in the deal, with estimated losses of about $400 million in fees (South China Morning Post). More broadly, the show of strength put in place by the government may have negative consequences on the entire domestic business ecosystem, already under strict control.

Meanwhile, Airbnb is ready to make its IPO filing public by next week, with the goal of going public in December (Reuters).

ESG investing

I have been writing about ESG investments for some months now, so it should not be surprising for you to read that, according to a recent report by NN Investment Partners, “around 15% of green bonds are still issued by companies involved in controversial practices”. As highlighted by the Financial Times, there are two ways to evaluate a green bond issuer: should it be valued for its overall ESG performance or the intended use of the green bond? This makes a big difference and there is not a clear answer yet. Ideally, both parameters should be taken into account to prevent a virtuous company from issuing green bonds to greenwash a traditional investment.

Jonathan Ford correctly notices that these investments should fund “activities that would not otherwise happen” to generate some positive impact (Financial Times).

The ESG industry counters that it is possible “to do well and do good” both at the same time. But there is no reason that doing good should deliver superior returns. If anything, it should be the opposite. Remember that impact investors should be funding something that does not seem sufficiently lucrative ex-ante to be backed by conventional financiers. Logically, then, you would expect them to receive “concessional”, or lower-than-market, returns.

The big picture

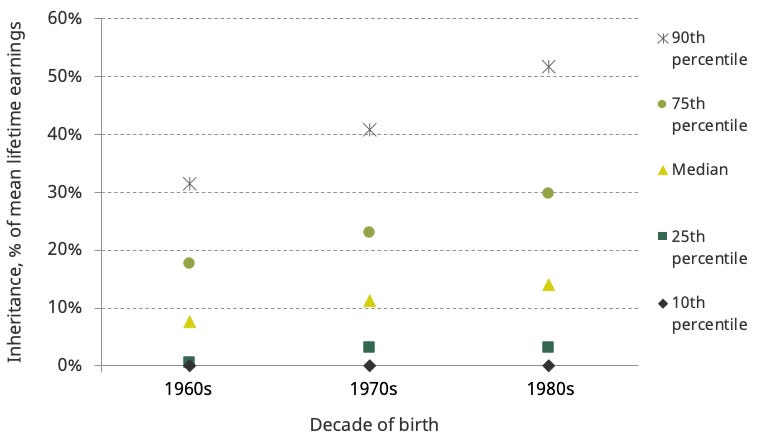

I received some interesting answers to last week’s issue regarding the small share of wealth owned by millennials. For more on that, take a look at the chart below, taken from a recent paper according to which inherited wealth will soon be “a much more important determinant of lifetime resources for today’s young than it was for previous generations”. This is nothing less than going back to some sort of feudal society: the life you live depends on your origins. Can capitalism afford that?

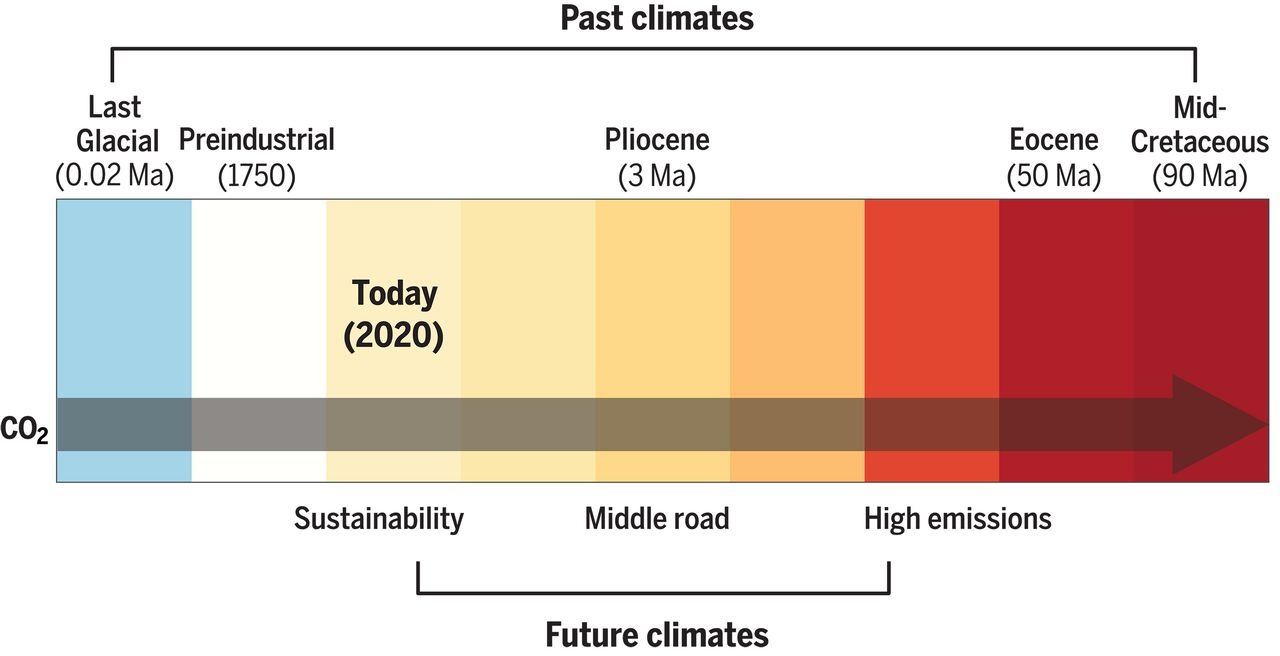

According to a new article, we need to improve our understanding of past climates to produce better climate change forecasts (Science). This is particularly relevant because “a major cause of uncertainties in climate projections is our imprecise knowledge of how much warming should occur as a result of a given increase in the amount of carbon dioxide in the atmosphere”. The picture below shows the correlation between the increase in CO2 and warmer climates in both past and future cases.

Thanks for reading.

As always, I am waiting for your opinion on the topics covered in this issue. If you enjoyed reading it, please leave a like (heart button above) and share Reshaped with potentially interested people.

Have a nice weekend!

Federico