🌌 Reshaped #16

Trump vs. Twitter, SoftBank in trouble, M&A during coronavirus, food supply chains, the EU recovery plan and much more

Welcome to a new issue of Reshaped, a newsletter for those who do not want to miss a thing about the huge transformations of our time.

This was a very intense week for tech, as the conflict between Donald Trump and Twitter will reshape the social media industry as we know it. I dedicated a separate section to the SoftBank Vision Fund case, which shows some interesting patterns on how venture capital manages crisis and failure.

Do not forget to share Reshaped with your friends and colleagues!

New to Reshaped? Sign up here!

News

⚔️ Donald Trump announced stricter rules for social media companies, accused of acting as monopolies to the detriment of conservatives (CNN). Specifically, Trump would amend Section 230 of the Communications Decency Act, which grants social media companies immunity from any legal action regarding the contents posted on their platforms. The announcement came a few hours after Twitter had tagged with a fact-check label one of Trump’s posts for the first time (BBC). In a recent interview, Mark Zuckerberg criticized Twitter, saying that “Facebook shouldn't be the arbiter of truth of everything that people say online” (Fox News). This opens a brand new chapter in the war between tech companies and the White House, but the ending could be very different from what Trump expects. Indeed, without immunity, social media companies would openly moderate the content on their platforms, acting as pure media companies (The Guardian).

🤝 Despite political concerns and economic turbulence, Big Tech companies have announced 19 M&A deals so far this year, the greatest amount since 2015 (Financial Times). The pandemic has caused a reduction in the valuation of many interesting tech startups, which could find in Big Tech an easy and somewhat unavoidable exit. Both in the US and the EU, regulators warned against opportunistic M&A activities by tech giants, which are emerging from the crisis stronger than ever and have enormous liquidity to spend on acquisitions. The news that Amazon is ready to purchase self-driving-car startup Zoox at less than its last private valuation of $3.2 billion is a perfect example of these dynamics (The Wall Street Journal). As highlighted on FT Alphaville, this is consistent with the previous investments in Aurora Innovation and Rivian, which is not only pushing Amazon towards an autonomous delivery fleet but also consolidating the industry.

[…] the self-driving car world will have to begin to consolidate. One, because there are arguably only two companies – Google and Amazon – that can support the sort of research and development intensity required without constantly returning to the capital markets. And second because a future where all cars operate on the same plain technologically, and can interact with the required state infrastructure, will require a level of standardisation within the industry which will naturally lend towards there being two active players at best. It is far more likely in 20 years the self-driving car technology suite – from software to sensors – resembles Boeing and Airbus’ stranglehold over the airliner space than the dispersed competitive landscape that currently exists.

🎶 Warner Music announced an IPO at Nasdaq for 13.7% of its common stock, which could value the company between $11.7 billion and $13.3 billion (The New York Times). Thanks to the diffusion of streaming services, the music industry is benefiting from a new positive wave. Despite the negative trend that started in the last quarter of 2019, IPOs remained resilient during the crisis (Financial Times).

📱 Instagram will share revenues from advertising with influencers and other content creators, starting with IGTV (The Verge). Precisely, creators will get 55% of the revenues from ads shown on IGTV and badges purchased by viewers of live videos. This is the first time Instagram shares its revenues with content creators, with the explicit objective of moving the latter from rival platforms (YouTube and TikTok above all) to the Facebook universe. However, this means Instagram will have to moderate content the same way YouTube does in order to avoid litigations with paying brands. If you see a link with the first news of this section, then you are probably on the right path. The debate on the future of social media companies is hotter than ever.

💶 The European Commission proposed a €750 billion recovery plan (€500 billion in grants and €250 billion in loans) based on join debt issuance (Politico). The proposal will now enter negotiations between member countries, which will have to vote unanimously on a final plan. The magnitude of the plan and the kind of economic governance it entails is unprecedented in the EU, which will use its own budget to issue bonds (The New York Times). It is also considering new fiscal policy — digital and carbon taxes above all — to finance the initiative.

🦄 A Vision Fund’s vision

In October 2016, the SoftBank Group announced the launch of a $100 billion investment fund aimed at supporting the most promising tech startups in the world. To amplify the magnitude of the new project, the biggest VC fund ever created, Softbank CEO Masayoshi Son called it Vision Fund. The vision of the management team and the backed founders would have been at the core of the fund, which committed to a long-term investment thesis and an authentic ambition to generate a positive impact in the world.

This announcement literally stunned the VC industry. SoftBank announced investments for $50 billion per year, with new funds raised every couple of years. The competitive advantage for SoftBank was evident: with a continuous stream of funds from financial and business partners, it would have been able to retain the best startups for future funding stages, while also benefiting from more bargaining power. If scale economies were relevant for startups, SoftBank was betting on the same mechanism for their financial backers.

However, there is an old saying in the startup environment: the more money you have, the more you are prone to making mistakes. It is easy to translate that into the VC world: a too easy fundraising process can lead to bad investment practices, especially if the dimension of the fund is a key component of its competitive advantage.

A few days ago, SoftBank provided a second shocking announcement: its results at the end of the fiscal year ended on March 31st. The company reported operating losses for $12.7 billion — the greatest ever recorded by a Japanese public company — and negative returns for the Vision Fund.

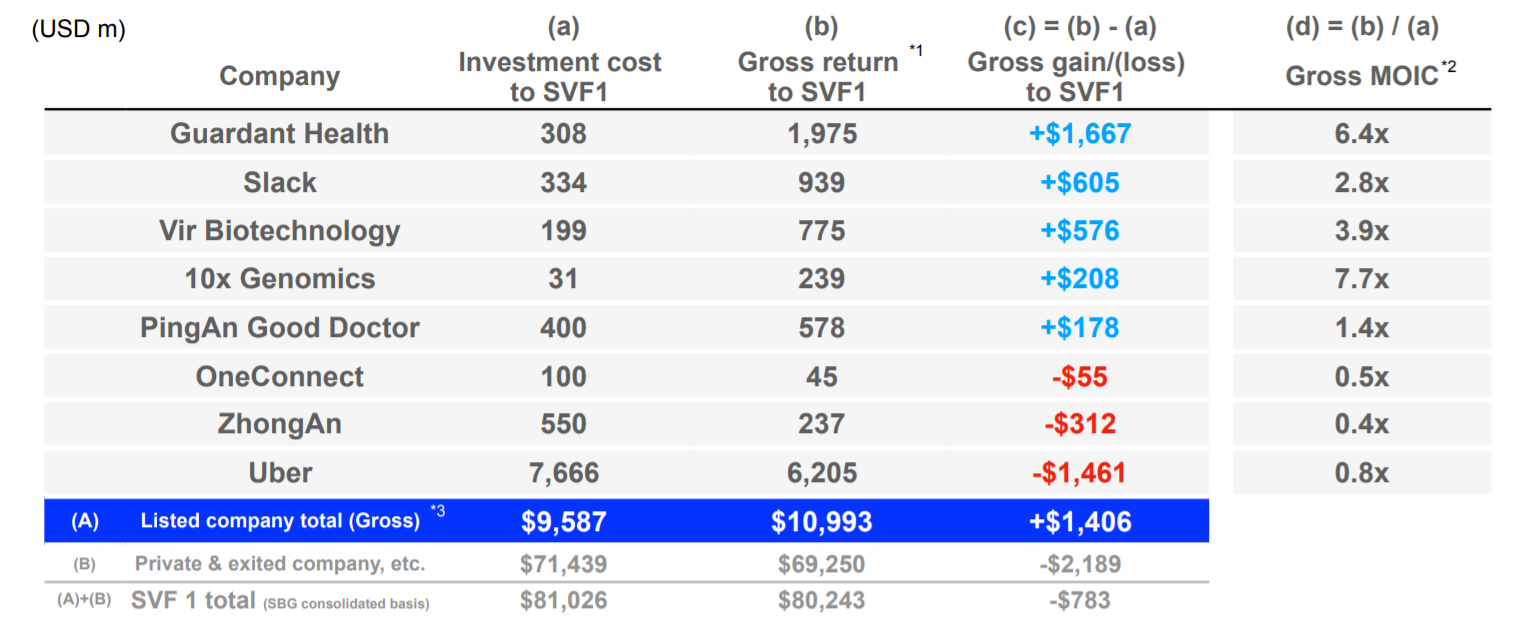

Masayoshi Son provided some explanations through a bizarre slide deck. It started (slides 3 to 12) by comparing the current pandemic to the Great Depression of 1929, explaining the impact of the current shock on various sectors and concluding that we are living an “unprecedented crisis”. Then, he reviewed the performance of the Vision Fund (slide 22), with 26 mark-up investments ($13.4 billion) and 47 mark-down investments ($14.2 billion), for a total investment loss of about $800 million. This means that the investment cost of the fund ($81 billion), far from generating returns for the investors, generated losses.

The following table (from slide 27) shows the performance of the eight listed startups financed by SoftBank. Overall, these investments generated gross gains for $1.4 billion, despite the negative impact of Uber on the performance of the portfolio. However, private and exited companies generated gross losses for more than $2 billion, which is why the total result is negative.

The performance of the fund has been heavily affected by the WeWork disaster and the current crisis of Uber. Masayoshi Son defined the investment in WeWork as foolish, with a valuation drop from $47 billion to just $2.9 billion in less than a year and a legal drama between SoftBank and Adam Neumann, WeWork’s former CEO, that further exacerbates the crisis of the company.

In addition, other investments in Asian markets are causing trouble to the fund. The Indian hotel chain Oyo was recently defined the next WeWork — which means, in short, a highly overvalued startup based on highly overvalued fixed assets and a highly overvalued founder. In parallel, the Chinese autonomous driving startup Didi, which is close to a new round worth $500 million from SoftBank, is facing the same problems that caused Uber to layoff thousands of workers.

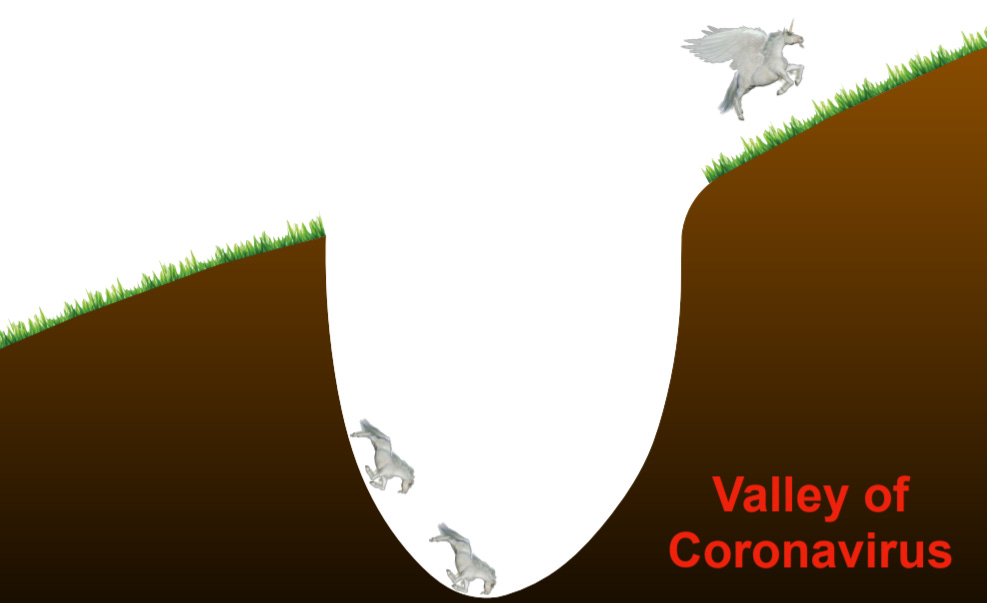

To explain the reasons for such a poor performance, Masayoshi Son concluded his presentation with a brief analysis of the impact of the pandemic on startups (slides 45 to 55). Basically, it goes like this: three white horses run on a hill, but a giant hole called the “Valley of Coronavirus” appears; two horses fall into it, while the third one becomes a unicorn and succeeds. Or maybe it succeeds and then becomes a unicorn — who knows? (Yes, those slides are quite embarrassing.)

While playing with horses, Masayoshi Son has to cope with these negative results. Investors pushed for SoftBank to sell shares of Alibaba — of which Masayoshi Son was an early investor — to finance a recovery plan. Curiously, it happened while Jack Ma, founder and former CEO of Alibaba, stepped down from the board of the Vision Fund. In the meanwhile, the conglomerate is ready to sell $20 billion of its T-Mobile shares, which are well-performing after the successful merger with SoftBank-backed Sprint.

In the meanwhile, Masayoshi Son has announced that the Vision Fund 2 will not be launched anytime soon, due to the poor performance of the first one. This second fund was announced about one year ago with the intent to focus more on profitability than growth, in order to avoid a new WeWork case. Hopefully, other VCs will learn the lesson as well, especially for capital-intensive industries that find it hard to survive without periodical capital injections.

In his presentation, Masayoshi Son listed six technologies that will reshape the post-coronavirus world: online meeting, food delivery, online education, online medical care, online shopping, and video streaming services. At the moment, SoftBank seems not very well positioned in those industries (see this investment tracker for more information), which are going to be more and more consolidated in the next months. The exception could be food delivery, especially if US regulators will allow Uber to acquire Grubhub. But, for sure, relying on gig-intensive food delivery would be a severe slap for a fund that wanted to change the world through futuristic technologies.

In the special issue dedicated to the future of venture capital, I wrote that I see the biggest potential in small, sector-specific funds. They have the expertise to forecast the future trends of their backed industries — something SoftBank was very bad at — and a genuine willingness to concentrate their investments on ventures that can redefine the standards of their sectors. This is what determines whether they will have the chance to raise another fund or not. Bigger funds tend to fall more often in what Byrne Hobart calls the “logo-hunting” phenomenon — VCs preferring to invest in good brands than good ventures.

Besides not having a clear vision, the Vision Fund was also weakened by the presence among its investors of sovereign wealth funds that have particular interests and carry geopolitical issues. The bad performance of the Vision Fund will reflect on the performances of those national funds, which is a relevant political aspect to take into account. In the end, being big seems to have provided little benefits to the fund.

Alternative perspectives

🚪 On Nature, Diane Coyle argues that economists should embrace multidisciplinarity in order to provide useful insights to policymakers in times of crisis.

Sadly, academic incentives work against people who are brave enough to cross into another discipline’s territory. Career, funding and publishing structures reward research into small, narrow questions, when the world has big, complex problems. Forbidding argot is prized; accessibility is viewed with suspicion. Universities, research institutes and laboratories are condemning themselves to irrelevance in future — and worse, now — if they do not break the shackles of departments and disciplines, and reward academics for policy relevance, as well as for basic research. This requires institutional reform, which is never easy and too slow for this crisis.

This is not a new argument, but the pandemic has shown all of its urgency. In particular, I think that two major trends will reshape the economist figure in the near future. The first is practical experience: as often argued by Branko Milanovic, too many economists live their entire life inside the academic world, with no real experience of the phenomena they study. This is going to change, as more and more economists will work closely with companies, public administrations, and international organizations at ambitious, mission-oriented projects. The second trend, as exposed in the article, is multidisciplinarity. I expect the emergence of many more university degrees that put together economics and field-specific subjects, from healthcare to energy, or other social sciences.

🌽 On The New York Review of Books, Michael Pollan analyzes the root causes of the US food supply chain weaknesses, which are strongly tied with the lax antitrust regulation introduced by the Reagan administration that resulted in agrifood monopolies.

Imagine how different the story would be if there were still tens of thousands of chicken and pig farmers bringing their animals to hundreds of regional slaughterhouses. An outbreak at any one of them would barely disturb the system; it certainly wouldn’t be front-page news. Meat would probably be more expensive, but the redundancy would render the system more resilient, making breakdowns in the national supply chain unlikely. Successive administrations allowed the industry to consolidate because the efficiencies promised to make meat cheaper for the consumer, which it did. It also gave us an industry so powerful it can enlist the president of the United States in its efforts to bring local health authorities to heel and force reluctant and frightened workers back onto the line.

A related argument is presented on The New Yorker, which focuses on the restaurant industry and its controversies.

🧩 On Palladium, Samo Burja argues that societies re-engineer themselves and determine the pace and the scope of technological change. This means that the huge transformations of societies and civilizations are not processes that automatically start when enabling technologies emerge. On the opposite, social technologies drive that change as a planned process.

An invention does not achieve adoption because of its mere existence, but only when it has found a stable socioeconomic niche. This is the difference between an invention and a technology. The archetype of the blacksmith cannot be reduced to any mere individual, nor to a set of tools, but personalizes an entire socioeconomic niche—one deeply entwined with our thought and life over millennia. These archetypes are even reflected in myths of settled societies instructing us how to think, how to live, and what dangers to avoid. When a technology is so deeply embedded in social practice, it can even survive the collapse of civilizations.

Other readings

🔦 On The Atlantic, Annika Neklason explains the relationship between the US civil war and conspiracy theories aimed at preserving slavery in the South.

🎤 On ProMarket, Matt Stoller explains in detail the impact of Spotify on the podcasting industry, a topic covered in the last issue of Reshaped.

🤑 In a post for the Institute for New Economic Thinking, Pirmin Fessler and Martin Schürz provide quantitative analysis on the effects of bailouts on income and wealth.

🧨 The Economist analyzes how the pandemic is rapidly reversing the positive trend in the fight against global poverty.

🛒 On The Guardian, Sirin Kale describes the pandemic under the perspective of supermarket staff.

📋 On Development Economics, André Roncaglia and João Romero argue that the pandemic has highlighted the need for a return to state planning. I agree with the principle, but there is a fundamental question we have to answer first: do our public institutions have the required skills and expertise for appropriate state planning? And, if not, how can we create incentives for talented people to join public institutions?

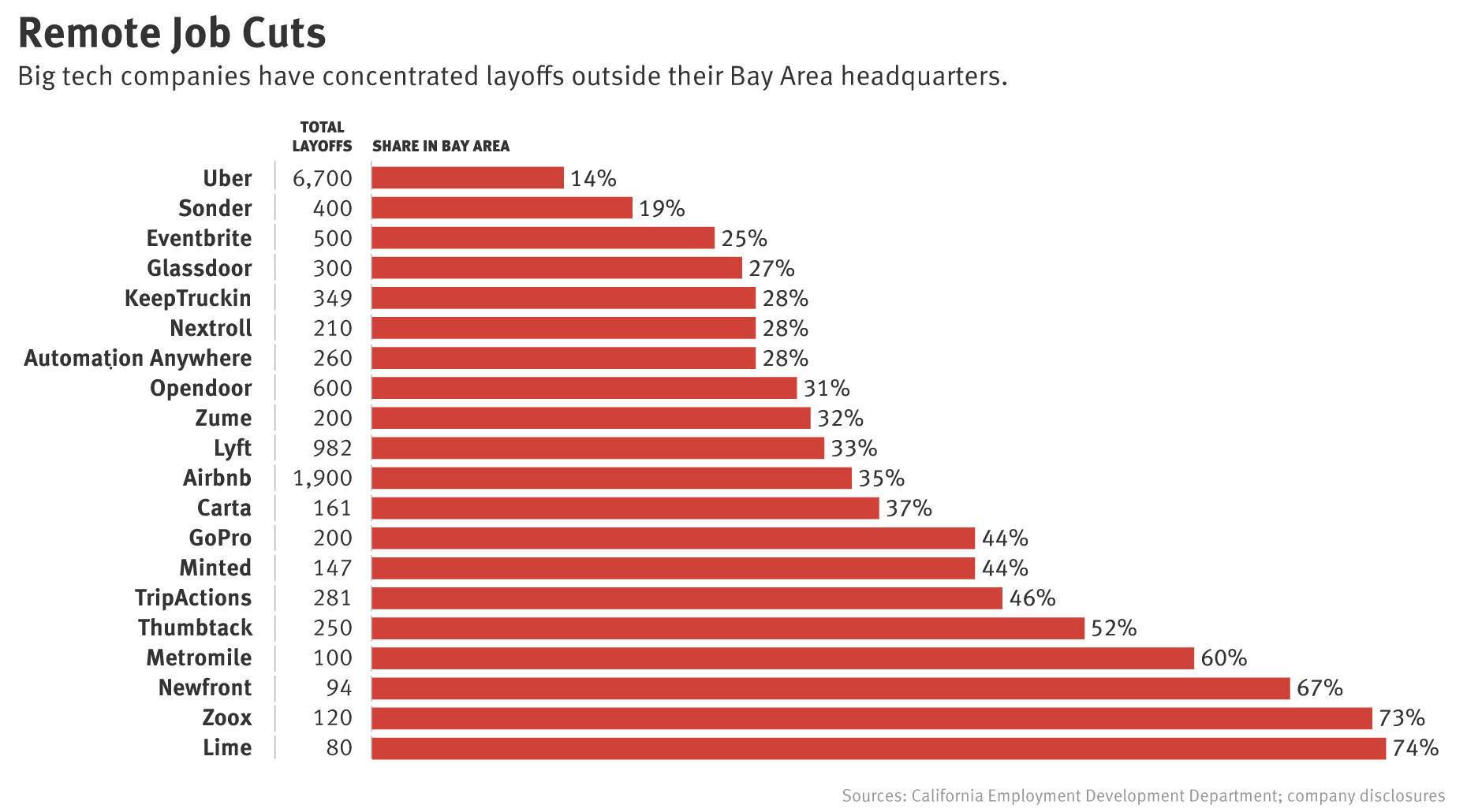

💻 On the British edition of Wired, Matt Clifford writes that remote working will finally cause the end of tech hubs like Silicon Valley, which would be replicable anywhere without a specific physical location. However, as reported by The Information, tech companies are concentrating layoffs far from San Francisco (see chart below), which contributes to preserving employment in the Bay Area.

Thanks for reading.

Please give me any feedback about this issue. If you enjoyed reading it, like and share Reshaped with potentially interested people.

Have a good weekend!

Federico