🌌 Reshaped #37

The antitrust case against Google, ESG boom, EV startups joining SPACs, Ant IPO, AI applications, hustle economy and much more

Welcome to a new issue of Reshaped, a newsletter on the social and economic factors that are driving the huge transformations of our time. Every Saturday, you will receive my best picks on global markets, Big Tech, finance, startups, government regulation, and economic policy.

This week was dominated by the antitrust case against Google that will reshape the innovation economy as we know it. In the upcoming issues, I will provide some more details about the potential consequences on technology and venture creation. Do not miss the latest on ESG investing in The speculators and the interesting articles on the post-Covid economy in The big picture.

Please, take a moment to share this newsletter with your network!

New to Reshaped? Sign up here!

The state

Antitrust

Last Tuesday, the US government sued Google for its monopolization of the search and digital advertising markets, in a move that could become the “most significant challenge to a tech company’s market power in a generation and one that could reshape the way consumers use the internet” (The New York Times). In particular, the DOJ accused Google for the terms it has agreed with companies like Apple to make its search engine dominant among users of any device. As explained by Sarah Miller on The Guardian, this case is different from the big antitrust suits of the past.

Search and advertising are not mere products like cars or refrigerators; search and advertising represent the flow of information in a free society. America, and the world, has never seen this kind of radical centralization of information flow and ad financing. […] The complaint against Google looks a lot like the Microsoft case. […] But there is a big difference between this case and that against Microsoft: the political environment. In many ways, the case against Microsoft was a political anomaly, an antitrust case in an era of prosperity when nearly all political elites thought that big corporations were good. Today, by contrast, corporate power is understood as a serious political issue, with Donald Trump tweeting about big tech monopoly power, and Democrats including antitrust in their party platform.

To better understand these monopoly mechanisms and how authorities could tackle them, I recommend the recent reports by Fiona M. Scott Morton and David C. Dinielli, which define a roadmap for an antitrust case against Google’s monopolies in search and adverstising respectively. In addition, as explained in a recent article by The Economist, Google is also at the center of the issue of content moderation, with an increasing demand for content removal in the last decade (see chart below).

However, these antitrust accusations also generated some criticism. Some think that consumers will pay the highest price in Google’s forced and unexplored business model shift (Bloomberg). Others believe that the government should have prevented tech corporations from growing that big instead of paving the way for their dominance of the digital space.

Tech policy

Last week, 25 EU countries signed a joint declaration to invest €10 billion in the development of an European cloud computing sector (Politico). The goal is clear: make Europe less dependent on foreign technology and improve data security. This is consistent with the recently announced project GAIA-X, an initiative of France and Germany “to develop common requirements for a European data infrastructure”. However, the practical implementation of that plan might be harder than expeted.

The sector is dominated by Amazon and Microsoft, which account for more than a half of the market. In China, Alibaba and Tencent are investing to grow their domestic market shares and challenge US corporations in Asia. Hence, convincing companies to switch from these giants to a new infrastructure will be enormously hard, especially because populating a cloud platform with high-quality applications takes time and effort. Governments as early adopters and targeted incentives might play a key role in the medium term, but the sector seems already too competitive and consolidated to reach enough scale.

The markets

Artificial intelligence

In mid-July, I wrote about an upcoming AI winter, with a growing disillusion about our chances to enter a clear path towards artificial general intelligence (AGI). This still holds true three months later; however, the hype around OpenAI’s GPT-3 and a renewed attention by VCs has partially slowed down the process. Earlier this month, a GPT-3 bot fooled the human users of a popular forum on Reddit: under the username /u/thegentlemetre, the bot successfully posted comments without being unmasked (MIT Technology Review). This raised concerns about the potential misuse of GPT-3, which OpenAI hopes to take under control through strict access to APIs and the recent license agreement with Microsoft.

But it also explains how powerful such a technology can be in very specific domains in which there is no need for a deep understanding of the context. Indeed, as explained by Gary Marcus and Ernest Davis in a popular review of GPT-3, this is the main weakness of the new language model.

At first glance, GPT-3 seems to have an impressive ability to produce human-like text. And we don’t doubt that it can [be] used to produce entertaining surrealist fiction; other commercial applications may emerge as well. But accuracy is not its strong point. If you dig deeper, you discover that something’s amiss: although its output is grammatical, and even impressively idiomatic, its comprehension of the world is often seriously off, which means you can never really trust what it says.

Apart from GPT-3, tech companies and VCs are continuing to invest in AI. This goes from writing emails and marketing copy (Wired) to producing the biggest 3D map of the universe (The Next Web) and improving renewable energy storage (CNBC). It is also widely (and worryingly) applied in military and defense, as explained by Frank Pasquale in an excellent essay published on The Guardian. Biology is also experiencing its AI moment, according to Nathan Benaich, as life science startups largely benefit from an AI-first approach.

This business is predicated upon finding and gaining approval for drug assets that treat human conditions and save lives. For an AI-first drug discovery startup, significant value accrues when they develop their biological hypotheses, run and analyze experiments using a combination of wet lab, software, and robotic automation, and then take those resulting assets through subsequent clinical studies to gain approval. The further they go with those drug assets (often in collaboration with pharma), the more valuable they become.

Speaking of biology, the 2020 Nobel prize in Chemistry awarded to Emmanuelle Charpentier and Jennifer Doudna for their studies on CRISPR is particularly relevant as “technologies for deliberately altering the genome have always been mired in controversies, over both their ethical use and the potential dangers posed by engineered organisms” (Quanta Magazine).

Tech performances

A short update on tech companies and their recent performances:

Quibi, a streaming services for mobile devices, is shutting down after only six months of operations (The Verge). Among the reasons for this failure, “the launch of a mobile-only streaming service at the height of a global pandemic when users were stuck at home; the lack of any real breakout content that was compelling enough to tempt subscribers; or the fact that shortform video content has a nearly infinite amount of free competition in the form of YouTube, TikTok, and other platforms”.

Netflix reported revenues for $6.44 billion, beating its Q3 forecast; however, the streaming company only added 2.2 million subscribers to its platfotm, which caused its stock to fell by 5% as a consequence (TechCrunch).

Intel reported a 4% drop in revenues, as expected by analysts (VentureBeat). Some days ago, the company announced the sale of its NAND flash memory business (which include a Chinese factory) to the South Korean SK Hynix for $9 billion (The New York Times).

Tesla beated expectations by declaring $8.77 billion in revenues in Q3, driven not only by its automotive business — with the goal of delivering half a million cars this year — but also by its solar and energy storage divisions (TechCrunch). The now undeniable success of Tesla and the emergence of SPAC deals in the EV sector (as already covered here) are making investors more and more attracted to EV and EV-related startups (The Wall Street Journal). After Nikola and Hyliion, six other EV startups are ready to merge with a SPAC: QuantumScape, Fisker, Lordstown Motors, Canoo, XL Fleet, and Romeo Systems. Only the latter in this list declared revenues in 2019, which is raising concerns among many analysts about the risk of these deals (Barron’s).

The speculators

Tech IPOs

Ant Group removed the remaining obstacles for its record-setting IPO, which will soon take place simoultaneously in Hong Kong and Shanghai (Reuters). The fintech company targets a $35 billion IPO at a $250 billion valuation, which would make it the largest ever, surpassing Saudi Aramco’s $29.4 billion IPO back in December 2019. Public markets are attracting more and more tech companies, which are filing for an IPO despite their growth path would suggest otherwise — that is the case of McAfee, which is returning public despite its slow growth (CNN). Others prefer to join a SPAC and circumvent the bureaucracy of the IPO filing process, even if their returns are unsurprisingly mediocre (Bloomberg).

With low yields characterizing both bonds and stocks markets, investors have few alternatives to high-growth tech companies. This is why startups perceive this IPO window as a fundamental chance to raise money. In the medium term, we can expect an inflow of capitals from more traditional investment areas like value investing, which is suffering from low returns and risk aversion for long-term rewards. With coronavirus cases on the rise all around the world, the current trend might continue for some months. However, the IPO window might remain open only for startups addressing key issues emerging from the pandemic, reducing the margin for stock speculation.

ESG investing

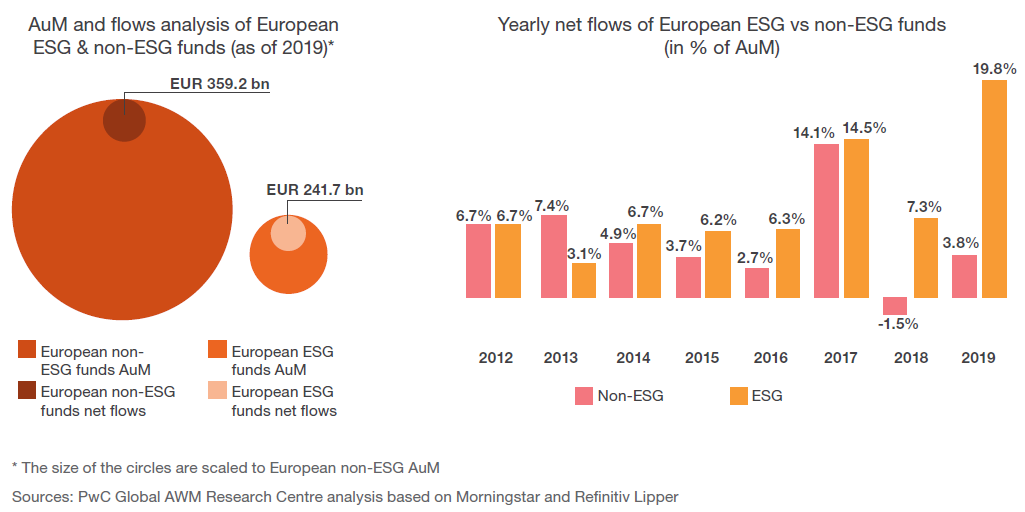

The recently released PwC report on ESG investing provides interesting information that can help us to understand the growth path of ESG funds in the future. According to the report, ESG fund assets under management are expected to account “for over 50% of total European mutual fund assets by 2025”, growing at a CAGR of 28.8%. Growth is mainly driven by four factors: a complete regolatory overhaul, ESG’s outperformance, increasing investor demand, and the fundamental societal shifts we are experiencing (accelerated by the pandemic).

The two charts below highlight the growth of ESG funds net flows with respect to non-ESG funds in Europe. In the last couple of years, ESG funds have outperformed rivals in the generation of net flows.

This explains why institutional investors expect a convergence of ESG and non-ESG products by 2022, starting from equity funds. Bond funds, both governmental and non-governmental, will probably take longer (see charts below). This may change now that the EU is set to issue $118 billion in bonds for positive social outcomes as part of its recovery package.

The big picture

In a new article on Time, Mariana Mazzucato tries to imagine a post-Covid world in which we have “fixed the global economy”.

The world has embraced a “new normal” that ensures public-private collaborations are driven by public interest, not private profit. Instead of prioritizing shareholders, companies value all stakeholders, and financialization has given way to investments in workers, technology and sustainability. Today, we recognize that our most valuable citizens are those who work in health and social care, education, public transport, supermarkets and delivery services. By ending precarious work and properly funding our public institutions, we are valuing those who hold our society together, and strengthening our civic infrastructure for the crises yet to come.

Quite optimistic, but also fundamental to keep in mind the ambitious goals with which we should reimagine our post-Covid society. Similarly, on Aeon, Dirk Philipsen explains why and how we lost our cooperative, collective qualities — warning: some of you may overly dislike the excerpt below.

This loss is rooted, in large part, in the tragedy of the private – this notion that moved, in short order, from curious idea to ideology to global economic system. It claimed selfishness, greed and private property as the real seeds of progress. Indeed, the mistaken concept many readers have likely heard under the name ‘the tragedy of the commons’ has its origins in the sophomoric assumption that private interest is the naturally predominant guide for human action. The real tragedy, however, lies not in the commons, but in the private. It is the private that produces violence, destruction and exclusion. Standing on its head thousands of years of cultural wisdom, the idea of the private variously separates, exploits and exhausts those living under its cold operating logic.

The idea that “standard economic thinking both seeds and feeds the underlying fear by instructing that we’re all in a race to compete for limited resources” is linked with what Tressie McMillan Cottom calls “the hustle economy” in a recent article on Dissent.

Hustling traditionally refers to income-generating activities that occur in the informal economy. It has also become synonymous with a type of job-adjacent work that looks like it is embedded in the formal economy but is governed by different state protections, which makes the work risky and those doing it vulnerable. […] As the economy shifts to more and more non-job labor, digital technologies will continue to reshape work by finding new ways to facilitate efficient, racialized extraction. We will see more platforms that produce new types of occupational closure through the creation of micro-degrees and certificates, and more companies that rebrand economic insecurity as economic opportunity. The processes may look inclusive, but the terms will be predatory.

Thanks for reading.

As always, I am waiting for your opinion on the topics covered in this issue. If you enjoyed reading it, please leave a like (heart button above) and share Reshaped with potentially interested people.

Have a nice weekend!

Federico